Don’t Blame Me, I Voted For the Other Guy

This is probably what most voters will be telling each other for the next two years, as our divided electorate more or less voted for more of the same leading up to the 2024 Presidential campaign (which unofficially starts like, yesterday!).

The anticipated “Red Wave” failed to materialize, as Democratic voters turned out in numbers. This is widely seen as a “repudiation in advance” of former President Trump’s expected decision to enter the race. While Republicans have apparently eked out a narrow majority in the House, the Senate is likely to remain split down the middle pending results of ballot counts in Nevada and Arizona, and a forthcoming runoff in Georgia.

Regardless of the outcome, the absence of a decisive shift in the relationship of forces between the two parties – despite widespread predictions that Republicans were on the way to a sweeping victory — virtually ensures a legislative slog for any proposals that might shake up the status quo in Washington.

Furthermore, that status quo remains blissfully ignorant of the grave threats likely to shake the market and the economy over the next two years.

It Will Be More of the Same, Until it Isn’t

If you follow Market Slice regularly, you’re already familiar with our main thesis. In a nutshell it’s this: there are too many things stretched to the breaking point for us to avoid a financial and economic disaster in 2023.

Diligent readers might want to go back through our posts from earlier in the year. Throughout 2022, we have warned that after waiting far too long to take action when it was clear that inflation was a problem, the Fed is now raising rates with reckless abandon.

We have not yet seen the full effects of this unprecedented increase in borrowing costs on the real economy. These typically take months to show up in hiring and spending patterns and the increases only started in June, with 225 basis points added to the Fed Funds rate since August.

When this radical anti-inflation measure hits home, the housing sector (a primary engine of the economy) is going to get slammed. We discussed this just three weeks ago in our article, Haunted Housing:

Several high-frequency data points for the week of October 9 indicate an ongoing deceleration in housing, including:

1. Pending sales down 28% YOY, vs a 25% decline last week, according to Redfin, a national real estate brokerage

2. Price declines on 7.9% of active listings, up from 7.7% last week and 5.0% in 2019

3. Mortgage purchase applications down 39% YOY, vs a 37% decrease last week

4. Median listings and sale prices 5% and 6% lower than their May/June peaks, respectively, though they remain higher YOY

Rising rates = declining affordability = lower sales = less confidence, job losses, and lower profits… in a business where builders are constantly at the edge of bankruptcy, even in boom times. Not a pretty picture. And as housing goes, so goes the economy.

And this is before the latest 75 bp hike, and with previous hikes still undigested in the market. So inflation, interest rates, and housing are one set of problems. But then there’s energy.

Without the power to override vetoes, there is no chance that pro-business Republicans will be able to head off the President’s energy policies. Biden affirmed his intention to put an end to oil drilling and attempt to cap prices this week. This provided a harsh dose of reality to consumers already struggling with rising heating costs heading into winter.

Coupled with the President’s politically inept promise to shut down coal mining in Pennsylvania, the “no drilling pledge” shows that we are heading into a period of tighter energy supplies, higher gasoline, heating oil, and natural gas prices.

This is not a good way to fight inflation. Food and energy may be exempt from core inflation calculations, but they are fundamental factors in the equation called “home economics.” When people are struggling to pay for food, energy, and rent, they don’t have money for other things. A recession is when there is no economic growth. Economic growth is fueled by consumer spending. You do the math.

“Business as usual” in Washington remains a cruel joke at America’s expense. As the seismic shifts we see coming finally do arrive, both our politicians and the vast majority of market participants will be caught unaware.

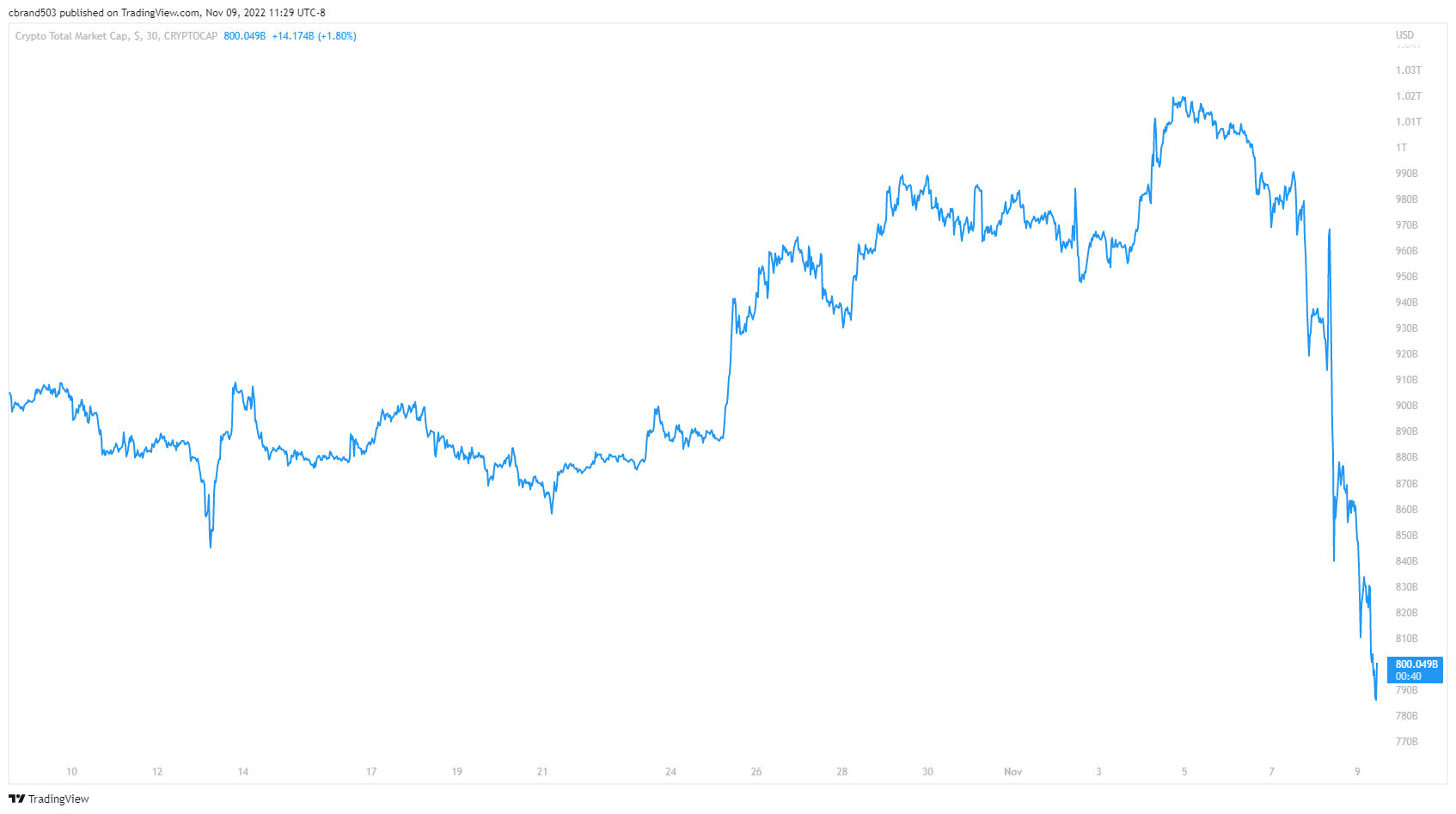

Crypto Crash Redux

There is a Ponzi scheme called crypto farming, where investors are paid a yield on non-revenue generating assets, and it is collapsing in the most dramatic fashion.

Crypto exchange FTX was hit with massive margin calls early this week. Within 24 hours it was on the verge of being bought out by giant competitor Binance.

However as of Wednesday morning, Binance will not be going through with the acquisition after looking at FTX’s books. This now leaves the vultures circling around the FTX corpse. Recent events have exposed questionable business practices that have been happening for months. As these are now being investigated, FTX investors stand to lose everything.

Among these investors is crypto wunderkind Sam Bankman-Fried, who has apparently seen his $16 billion-plus net worth shrink to barely $1 billion in the course of a few days.

Of course, the entire cryptocurrency market has been devastated (again). The word “contagion,” last heard with the Terra/Luna disaster back in May, is once again in the wind. Bitcoin has plunged past the $17,000 level, and the total mark cap of the crypto sector has fallen off the table.

While crypto bulls regroup and prepare the next round of coin-splaining, what we highlighted in September remains. At this stage, cryptocurrency investing is a purely speculative venture. And this bound to suffer losses as we move into an increasingly risk-off market environment.