Is the trading party over? We discuss the end of stimulus, rise of inflation, and more in this week’s issue!

Crashing from the stimulus sugar high

Two years ago, the U.S. government and the Federal Reserve embarked on the most ambitious stimulus program ever.

Under pressure from the COVID pandemic and the measures taken to control its spread, $5 trillion (that’s 5,000 billion… a tidy sum by any measure!) was distributed to American consumers and businesses.

At the same time, the Fed extended its policy of maintaining near-zero interest rates, providing a gusher of easy money to the banking system, along with Quantitative Easing measures designed to strengthen the balance sheets of financial institutions, and a host of similar measures.

This stimulus succeeded in staving off an economic crisis during the lockdowns and extended closing of the economy supposedly required to deal with the pandemic. But not without a price.

The unintended result of this free money policy was not unlike what you see at a kids’ birthday party, with unlimited cake, candy and soda for all.

And the hangover is only starting to be felt.

It’s easy to criticize the government and the Fed for their egregious policy errors, and even more for the stubborn refusal to recognize that they would inevitably lead to the inflationary consequences we are seeing today.

Nonetheless, our intention today is not to condemn the Fed… they’ve gotten their share of criticism already. Rather, we want to examine the most likely consumer response to recent economic developments.

With talk of a recession now dominating the public conversation, it’s worth looking at how American consumers are likely to respond in the face of an economic downturn.

This is particularly important because the official story is that the economy remains strong. Powell and Biden insist that there is no sign of a recession in sight…while some (including this publication) insist that we are already in one!

According to YCharts, consumers are not so sanguine about the economic outlook:

US Index of Consumer Sentiment is at a current level of 50.20, down from 58.40 last month and down from 85.50 one year ago. This is a change of -14.04% from last month and -41.29% from one year ago.

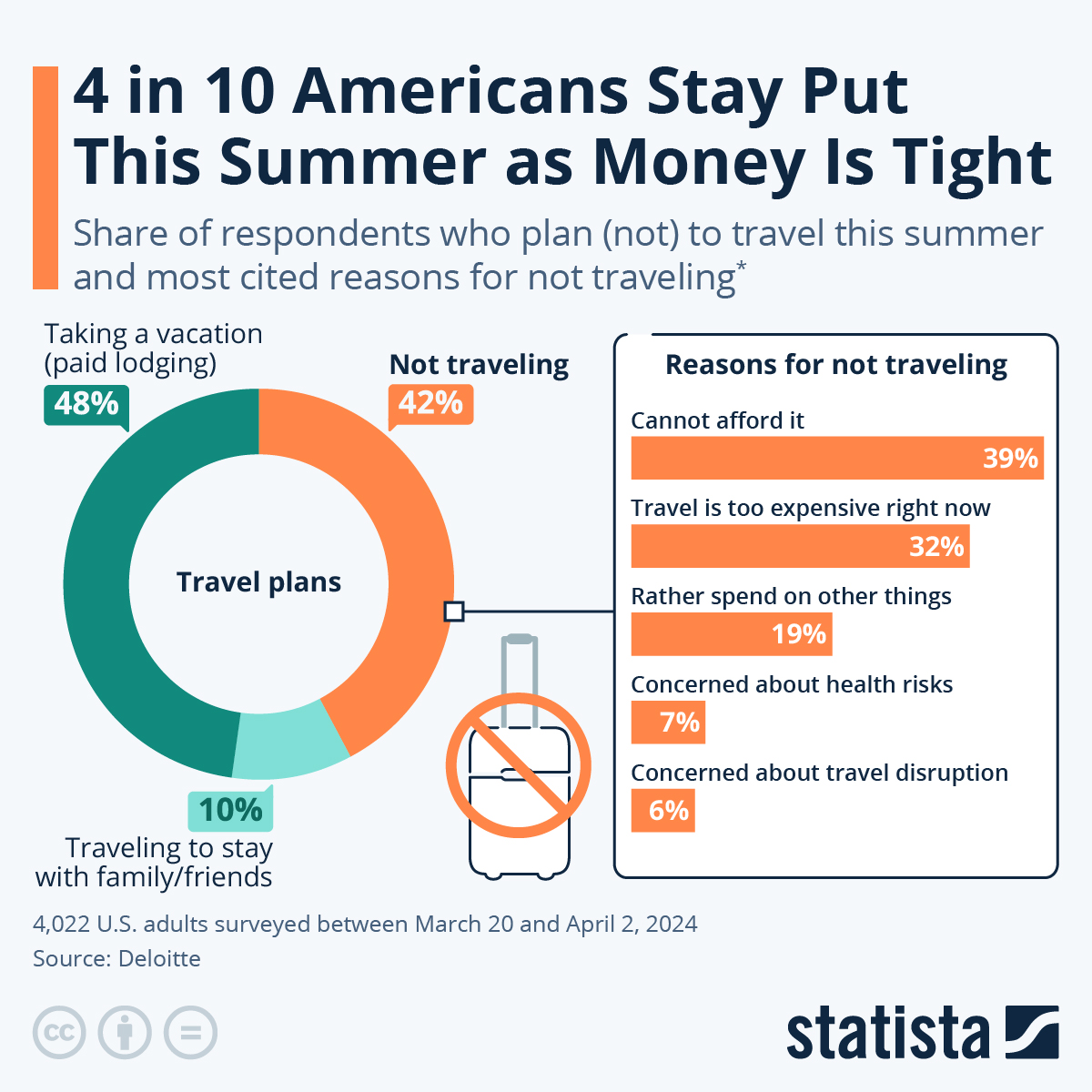

And here’s one more indication at all is not rosy for consumer spending:

Link and credit here per Statista

{kind=link}

If travelers stay home, it will impact the outlook for a host of industries desperately in need of a bounce-back year. Just another indication that Biden’s hopes for avoiding recession are unlikely to be realized.

What do you think? Are we heading into a recession, or in one already? Or is it possible to avoid a serious economic downturn? You can discuss this with a knowledgeable member of FFR Trading’s Strategy Team…we’ll help you figure out what today’s climate means for your investment and trading goals. Call (800) 883-0524 to schedule a no-risk strategy call.

Look Out for These Corporate Bogeymen

Three very dark clouds are on the stock market horizon, threatening to wash out any hopes for a “soft landing.”

- Inventory surpluses. “Retailers have an inventory problem,” according to org. With supply chain slowdowns over the past 18 months, many stores are now overstocked with items ordered during the shutdown. Now, just as workers are returning to the office and consumers are tightening their purses, retailers like Target and Walmart are sounding alarms about excess inventory. This could necessitate price cuts, and hurt profitability.

- Margin squeezes. In addition to inventory woes, companies face several other challenges to bottom-line profitability. As materials and transportation costs remain stubbornly high and buyers sit on their wallets, businesses are challenged to maintain sales (revenue), and are forced to compete on price, which lowers their margins (profits). So far earnings and profitability have remained relatively buoyant – although many companies did miss earnings estimates in the 1st Some commentators are concerned that 2nd quarter earnings reports could be considerably worse, and that bleak forward guidance for the rest of the year will drive equities prices lower.

- Rising interest rates. Back in January we wrote about the Fed’s double bind… on one hand, they need to raise interest rates to slow inflation, but on the other, increasing rates means higher cost of debt service, which could sink countless “zombie companies” – businesses that can barely make the interest payments on their debt, even at current super-low rates. Even healthy companies generally carry a percentage of their debt at floating rates, which means that as rates go up, so does the short-term cost of servicing their debt. This is another factor that threatens cash flow and profits…meaning it is another factor threatening to send stock prices lower.

If consumers are hurting and unwilling to spend, and companies are already feeling the pain of economic slowdown, is there any reason to expect a turnaround any time soon?

These are just some of the reasons we say a recession is already here…and just like with “transitory inflation,” the Fed is woefully behind the curve in seeing what is actually going on in the real world.

That’s the problem with institutions run by lawyers, corporate shills, and government yes-men. It’s no surprise that they are so consistently wrong… what would be really shocking would be if they somehow managed to fix the fine mess they’ve gotten us into.

Your financial future is no laughing matter. If you aren’t positioned to profit from this recession, you need to talk with FFR Trading right away. Call our Strategy Team at (800) 883-0524 today, or click below to schedule a free portfolio evaluation.

What About Commodities?

Overvalued stocks and pressured bonds are two of the “storm fronts” converging in the markets today. The third is commodities,

When President Biden, speaking in Poland last week, warned that food shortages are “going to be real,” the major media barely noticed. However, this somber message could impact the lives of millions around the world, and in the United States.

Food shortages here might mean inconvenience, or, for some, real hunger. But for those in the poorer corners of the planet, it could mean literal starvation.

Combined, Ukraine and Russia account for around 30% of the world’s wheat exports. The war has already constrained these supplies, and continuing tension – whether the shooting end soon or not – are likely to exert a long-term upward pressure on wheat and other grain prices.

The Price of Money

It isn’t widely understood, but interest rates are actually the borrowing cost for everything that makes our capitalist system run. In a very real sense, the rates paid on loans, from bonds to mortgages to credit card bills, are literally the price of money.

The simple fact is that interest rates are the most important prices in the economy, not only here at home, but globally.

Everything — from financial institutions to the real estate market to manufacturing and distribution to service industries — is impacted by changes in rates.

Recently, Nick Giambruno made a key observation in Doug Casey’s International Man daily email latter. Here’s what he wrote: “Today, we are on the cusp of a rare paradigm shift in interest rates. Such changes take decades—or even generations—to occur. But when they do, the financial implications are profound.”

Market Slice note: Giambruno provides this chart from the Fed showing historical yields on the 10-Year Treasury Note, and the chart below, which tracks the past 10 years of yield changes. Notice that our current 10-year high is still far below the historic median, depicted on the red line above.

Remember, interest rates are the price of money. They are the most important prices in all of capitalism. Yet they’re controlled by a politburo of central planners at the Federal Reserve, not set by the market like any other price.

It’s strange that many people thoughtlessly accept this as “normal.” In reality, the Fed is engaged in a massive price-fixing scam… and nobody seems to care.

While the Fed exercises undue influence over interest rates, other significant factors are at play here. And they all point to higher interest rates.

Together, they’re ushering in a once-in-a-generation shift that is both unstoppable and imminent.

To summarize, here are the five reasons to expect higher interest rates:

- Inflation is out of control. Even the government’s official inflation statistics—which understate the situation—are far above current interest rates.

- The federal government must issue a flood of new Treasuries to finance multi-trillion dollar deficits—which are here to stay.

- Sanctions are eroding confidence in the US financial system.

- Foreigners aren’t buying as many Treasuries.

- The Fed is tightening.

When you connect all the dots, I think it’s clear we are starting a new long-term cycle, with rising interest rates and a bear market in bonds. That will have enormous implications for the economy and the stock market.

The implications of this historic cycle reversal are immense. In next week’s issue, we’ll take a closer look at how the twin pressures of high inflation and increasing yields pose grave dangers to your financial future.

Don’t wait until it’s too late to protect yourself from the coming interest rate crisis. Recession plus inflation – stagflation –takes a brutal toll on conventional investing strategies. FFR Trading’s clientele continues to profit with well-placed commodity trades, short positions in the stock market and on the equities indexes, as well as some carefully selected longs, option spread strategies, and more. Put out team of professional traders to work on your trading account…call (800) 883-0524 today, and speak with a Strategy Team professional

Stay in the loop with more frequent investment and trading updates to have the tools to better manage your investment portfolio! Make sure to check us out on Instagram, Facebook, and Twitter! Happy Trading!